Products are selected by our editors, we may earn commission from links on this page.

Wealth management has always been sold as a personal relationship. Your adviser knows your goals, tracks your portfolio, and calls when the market moves. According to a Bloomberg report, that relationship is being automated out of existence for anyone whose liquid assets fall below a specific threshold. The personalized service was never equally distributed. Now the industry is making that official.

The dividing line, according to Debasish Patnaik, a partner at McKinsey and Company, is roughly $1 million in liquid assets. Clients below that threshold are referred to internally as “mass affluent,” a term that signals something specific to the firms managing their money: these clients are profitable enough to keep but no longer valuable enough to staff. The reports, the check-ins, the portfolio reviews — those are being handed to AI. The adviser is being reassigned.

“The mass-affluent client now gets something close to private-banking quality from AI,” Patnaik told Bloomberg. That framing matters. It is not that service is being cut. It is that the same output is being delivered at a fraction of the cost, by software, without a human in the loop. For the firms, that is an efficiency gain. For clients accustomed to working with a person, it is a structural change that most have not been told is coming.

This article was created with the assistance of AI and reviewed by our editorial team for accuracy and clarity.

The Wealthier the Client, the More Human the Service — Wealth Management Is Splitting Into Two Tiers

The automation affecting mass affluent clients is not spreading evenly across wealth management. According to the Bloomberg report, the industry is moving in two directions simultaneously: replacing human contact at the lower end while deepening it at the top. The result is a system where the quality of human attention you receive is determined by how much money you have, more explicitly than ever before.

For clients with significant assets above the mass affluent threshold, firms are building out highly personalized services that AI cannot replicate. Patnaik told Bloomberg that wealth managers serving this tier will need skills including managing succession events, navigating family dynamics, advising on inheritance decisions across family members, and providing direct emotional support when markets decline. These are judgment-dependent, relationship-intensive tasks. Patnaik said firms will “weight hiring heavily toward” candidates who can perform them.

The jobs being created at the lower end of the market look nothing like traditional wealth management roles. Patnaik described a new category of positions firms will need to fill: specialists in behavioral data science, personalization architects, and what he called “human-in-the-loop oversight professionals.” These are roles built around managing the AI, not advising the client. The bifurcation is not just in service delivery. It is in the workforce firms are building to deliver it.

Citi Is Already Deploying AI Chatbots for College Savings Advice and CIO Emails Written by Algorithm

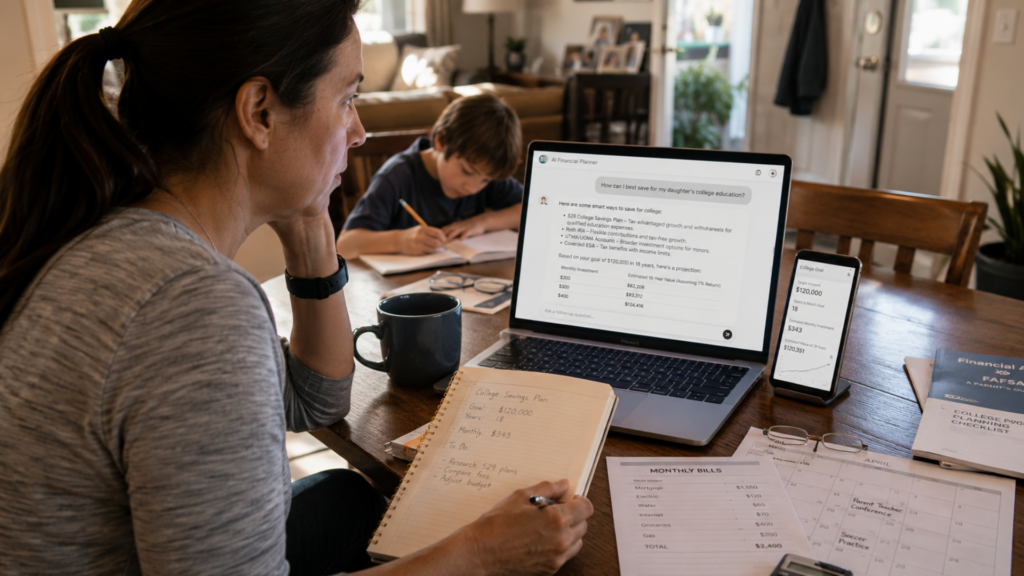

At least one major financial institution is not waiting for the industry to settle on a standard before moving. Citi has begun rolling out AI-backed tools for its wealth management clients, according to the Bloomberg report. Among them is a chatbot designed to guide clients through decisions about their children’s college savings, and a system that can draft communications from the firm’s chief investment officer and translate them into personalized client language automatically.

Joe Bonanno, Citi’s Head of Wealth Intelligence, framed the push in terms of client retention. “Engagement keeps clients happier and stickier,” he told Bloomberg. The logic is that more frequent, AI-generated touchpoints maintain the feeling of an active advisory relationship, even when no adviser is actively involved. For the firm, more engagement means lower attrition. For the client, it means more contact with software presenting itself as service.

The college savings chatbot is a telling choice of product to highlight. It is the kind of decision that feels personal and consequential to the client, tied to a child’s future and a family’s financial planning. Routing it through an AI tool reflects the broader bet these firms are making: that the emotional weight of a financial decision does not require a human to address it, as long as the interface feels responsive enough to feel like one.

The Industry Just Gave a Name to Clients It No Longer Wants to Staff, and Most Americans Fall Into That Category

The term “mass affluent” is doing significant work in this story. It sounds like a compliment. In practice it is a classification that tells a firm’s internal workforce where to stop spending human time. Clients in this category hold real assets, carry real financial complexity, and have real stakes in the advice they receive. The label does not change any of that. It just signals that their account balance does not justify a person picking up the phone.

The threshold being drawn at $1 million in liquid assets is not a fringe cutoff. The majority of American households fall well below it. According to the Federal Reserve’s Survey of Consumer Finances, median family wealth in the United States is a fraction of that figure, meaning the clients being shifted to AI-managed services represent not an edge case but the overwhelming center of mass in American personal finance. The segment the industry is automating away from is the segment most people belong to.

What is being automated is not just a task. It is the judgment that comes with knowing a client’s full picture: their income instability, their family obligations, their risk tolerance under real pressure. AI tools can parse a portfolio and generate a summary. They cannot tell the difference between a client who is financially fine and a client who is one job loss away from liquidating everything. That distinction has always been the actual value of a financial adviser. It is also the first thing the industry is removing from the people who can least afford to lose it.