Products are selected by our editors, we may earn commission from links on this page.

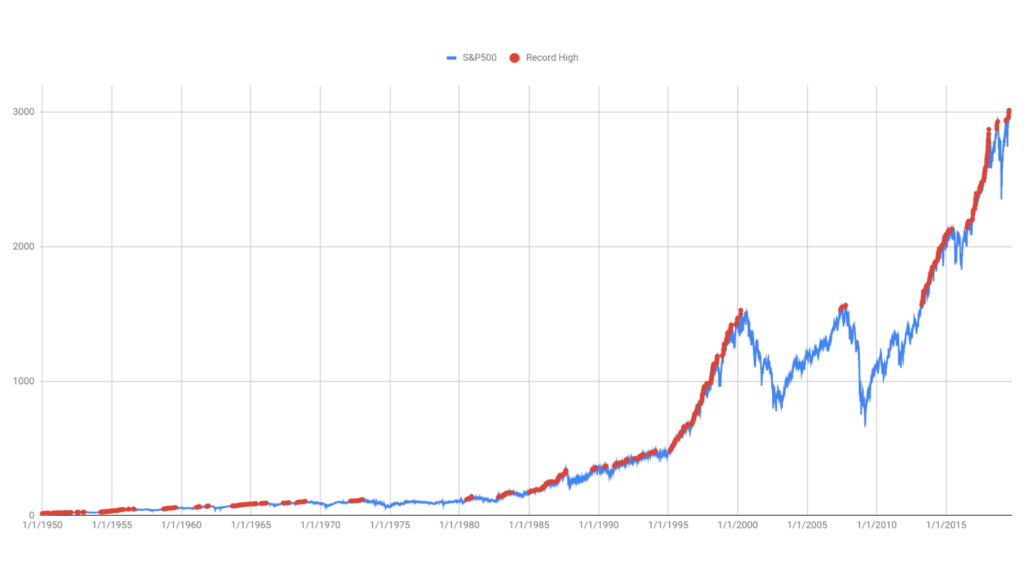

The S&P 500 just hit a record high on the same day consumer confidence sank to its lowest reading since 1952. Tech stocks are surging on trillions in AI spending. Everywhere on financial radio, the conversation is the same two letters: AI. For a generation of veteran analysts who lived through the dot-com crash, none of this feels new. It feels, uncomfortably, like the final months of 1999. And the last time this song played, the market lost nearly 80% of its value.

“If you weren’t trading in 1999–2000, then you’re in luck. This is what it was like. Now you can experience it.” — Helene Meisler, market technician

A Generational Divide on Wall Street

The debate over whether AI stocks are in a bubble tracks closely with age. According to Steve Sosnick, chief strategist at Interactive Brokers, investors who traded during the dot-com era are experiencing visceral flashbacks, while younger traders have grown up in a market where every dip eventually recovered. These newer investors have never personally watched a mania unravel. That generational gap shapes not just how people feel about risk, but how they respond to warning signs that older hands recognize immediately.

A Rare Pattern That Has Appeared Only Four Times in History

In May 2026, the S&P 500 reached a record high even as 5% of its components simultaneously hit 52-week lows, a sign of extreme concentration in a handful of tech names propping up the broader index. According to analyst Jason Goepfert, that combination has occurred only four times in market history: July 1929, January 1973, December 1999, and now. Three of those prior instances preceded significant crashes. Research from IntuitionLabs confirms the five largest companies now hold 30% of the S&P 500, the greatest concentration in half a century.

This Time, the Companies Actually Make Money

Optimists point to a critical difference from the 1990s. In the dot-com era, nearly three-quarters of publicly traded internet companies carried negative cash flows. Today’s AI leaders, including Nvidia, Microsoft, Alphabet, and Meta, are generating substantial profits. S&P 500 earnings grew roughly 27% year-on-year in Q1 2026. The technology sector’s forward price-to-earnings ratio, while elevated, still sits well below the extreme multiples seen in early 2000. Real earnings, not hype, are driving much of the rally.

The Spending Is Staggering, and That Cuts Both Ways

America’s largest tech companies pledged a combined $320 billion in capital expenditures for 2025 alone, mostly for AI data centers. Fortune reports that global corporate AI investment reached $252 billion in 2024, growing thirteenfold since 2014. Bulls argue this physical infrastructure represents durable assets, unlike the dot-com era’s marketing spend. But skeptics warn that if demand projections prove too optimistic, billions in hardware could sit idle. The telecom buildout of the 1990s made the same promise. It didn’t end well for those who bet on it.

The Rally Has No Central Bank Safety Net This Time

In 1999, the Federal Reserve flooded the financial system with liquidity to guard against potential disruptions from the Y2K computer bug. That flood of cash poured fuel onto the tech rally, making the eventual crash far worse when it came. Today’s AI rally is advancing without that kind of monetary support. The Fed has not cut interest rates since late 2025 and may not do so until 2027. Bond yields are rising, oil prices remain elevated, and inflation is climbing. The market is rallying against the current rather than with it.

War, Oil, and a Market That Shrugs at Bad News

Since the US-Israel military action against Iran in early 2026, equity markets have repeatedly rallied on any hint of a ceasefire or agreement to reopen the Strait of Hormuz. The concerning pattern, according to Sosnick, is that the market never suffers when those deals fail to materialize. Meanwhile, the University of Michigan Consumer Sentiment Index dropped to 48.2 in May 2026, its lowest reading in the survey’s 74-year history. A market climbing higher while consumers feel historically pessimistic is a disconnect that few analysts can explain away.

Michael Burry Is Sounding Familiar Alarms

Michael Burry, who famously anticipated the 2008 housing collapse, has taken bearish positions against Nvidia and Palantir, comparing the current AI frenzy to the closing months of the 1999 bubble. In a post on his Substack, he drew a pointed parallel between Federal Reserve Chair Jerome Powell’s assurances about AI profitability today and Alan Greenspan’s 2005 dismissal of any housing bubble. Burry acknowledges his track record of early warnings is uneven, adding, “I am now a meme for the number of times I have called a crash.” But he is not backing down.

AI Is Already Changing Business, and That Matters

Unlike the speculative dot-com era, when companies burned through cash chasing an idea, AI is already producing measurable productivity gains across multiple industries. Roundhill Investments analysis shows that roughly 78% of the tech sector’s recent gains have come from actual earnings growth, not multiple expansion. During the dot-com bubble, the reverse was true: 314% of gains came from inflated valuations untethered from profits. Analysts note that a reckoning may still come, but the starting point is fundamentally stronger than it was in 1999, leaving the outcome genuinely uncertain.

The Rhyme Without a Resolution

The honest answer from most analysts is that no one knows how this ends. The companies driving today’s rally are more profitable than their dot-com predecessors. The technology is real. But the concentration of market gains in a handful of names, the widening gap between stock prices and economic reality, and the momentum-driven logic of “stocks go up because stocks go up” are patterns that precede crashes in the history books. Whether 2026 becomes 2000 or simply a chapter in a longer boom may depend on something no analyst can predict: when the mood changes.